MC Students React to the Rising Tuition Rates and Student Loan Forgiveness

The recent release of President Joe Biden's student loan forgiveness causes evaluation of rising rates in higher education.

President Biden recently made good on his administration’s promise of aiding in the student loan debt crisis facing many lower-middle class borrowers of the U.S. Department of Education’s (ED) federal student loan program. The president announced a three-part plan which includes one-time loan forgiveness up to $20,000 if certain requirements are met, as well as a final extension of the student loan repayment pause, and “mak[ing] the student loan system more manageable for future and current borrowers” according to the ED’s official website.

To qualify for federal student loan relief the following qualifications provided by the Department of Education are outlined:

If one’s annual income is below $125,000 (for individuals) or $250,000 (for married couples or heads of household)

If one received a Pell Grant in college and meets the income threshold, one is eligible for up to $20,000 in debt cancellation

If one did not receive a Pell Grant in college and meets the income threshold, one is eligible for up to $10,000 in debt cancellation

About eight million borrowers will receive automatic relief, while anyone else is encouraged to fill out an application that is to be set up by early October by the department. Enrollments for the loan relief after November 1, 2022, will not be eligible. The department also advised borrowers to apply before November 15 in order to receive benefits before the loan payment pause expires at the end of the year.

An estimate of $300 billion and $980 billion in national debt will be accrued over a ten-year period on account of the loan debt budgeting in the federal treasury, according to UPenn’s Penn Wharton Budget Model for forgiving student loans, published on August 23. The Model also evaluated about 70% of debt relief being transferred to borrowers in the top 60% of the income distribution.

Mixed opinions from either side of the political spectrum have led to debate among the nation’s and state’s lawmakers. Current and former MC students, to whom this legislation directly pertains, also added their insight.

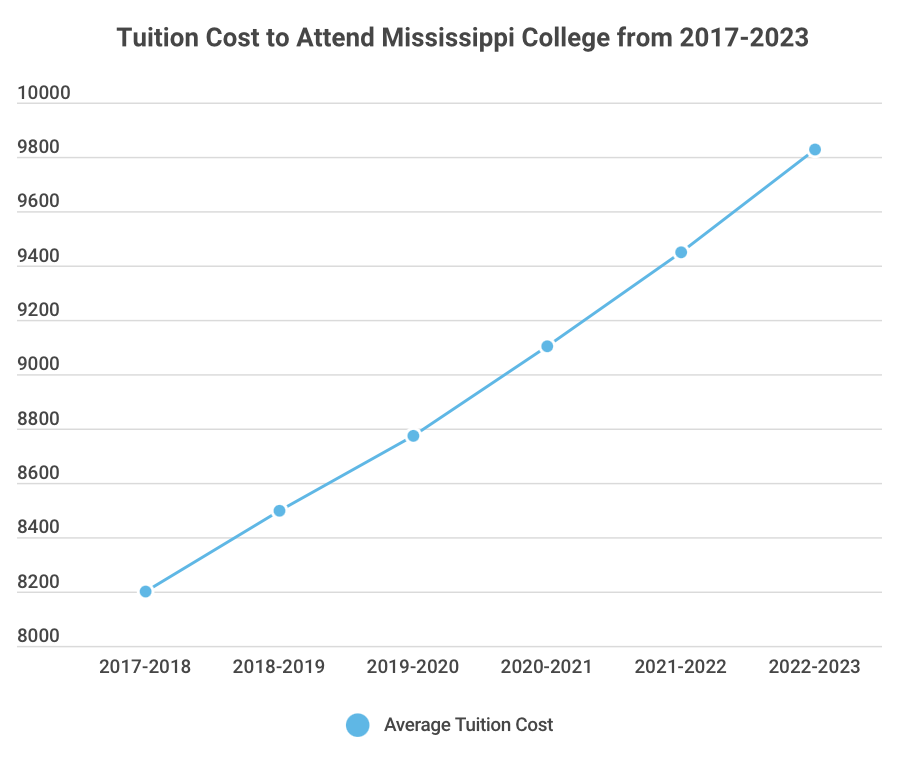

For a Mississippi College undergraduate student taking fall or spring semester classes with a number of 12-18 hours total, qualifying as a full-time student, tuition fees alone will cost roughly $10,000 in addition to living expenses, technology and registration fees, etc. On average without financial aid, in the academic year of 2022-2023, an undergraduate student’s fee bill, who is taking 17 hours of course work and living in non-premium, double occupancy campus housing (including the cost of a 19-meal plan), can pay up to almost $16,000 per semester. In addition to this, tuition costs at the university have risen upwards of $1,600 in just six years.

However, the university’s Institutional Data set states that in 2020-2021 “99% of Mississippi College's full-time beginning undergraduates received grant/scholarship aid.” With this in view how affected by student loan debt are Mississippi College students?

For a public speaking class last semester Liliana Talazac, a junior Public Relations Major, prepared an extemporaneous speech about a topic of interest to her. She chose to speak on “why student loans are dumb,” the namesake of her speech. Growing up the daughter of a financial advisor father, she was raised with terms like “fiscal responsibility” and “financial literacy” floating around their household.

Within her assignment, Talazac cited a piece of her own primary research in which she asked her public speaking classmates to participate. She found that for a classroom of 21 students, with an average of any one student paying $100,000 after the completion of their four-year degree, the potential debt accrued by the students would total approximately $2 million as they were hearing her speak on student loans.

“I opened my speech with those calculations because it’s simply unacceptable how expensive higher education is. The reason for that is that the institutions we attend for college should be held accountable for ensuring the quality of the education we receive by fairly paying the faculty they employ and the systems under them function and process as they should.”

No one wishes for people to accumulate crushing amounts of debt, but is this plan an effective way to lessen the load for the most vulnerable people affected by student loan debt?

“In terms of fairness and ethics, I’ve been left to wonder if this is actually a solution. On the surface level, it seems to just be slapping a band-aid on top of a gushing wound,” said Lakelynn Fancher, a junior Marketing major. “I feel empathy for those who have gone before me and have suffered to not only get an education but also be able to work enough to pay off the debt that it took to get there. However, I don’t think the past should hold us back from prosperity in the future.”

One Mississippi College alumni was weary of legislation like this one due the skewed message it may send to current students and young adults.

“For me, I paid off my student loans as fast as I could and then got into all of that. When the first real bill you have a young adult is simply forgiven as the plan is suggesting may be the case for many young adults, that is an unrealistic precedent set for future debt. Not every bill will be ripped up and thrown out,” said Daniel Henderson, an Accounting graduate of the class of 2011.

“I treated my student loans as an obligation. I don’t think the answer to outstanding debt is more debt. We need to be a society that encourages living within your means. That can look like graduating college with a degree that will cost you $100,000 in loan debt and get you a job that pays $50,000 a year and not being able to afford a house or car note right out the gate into adulthood.”

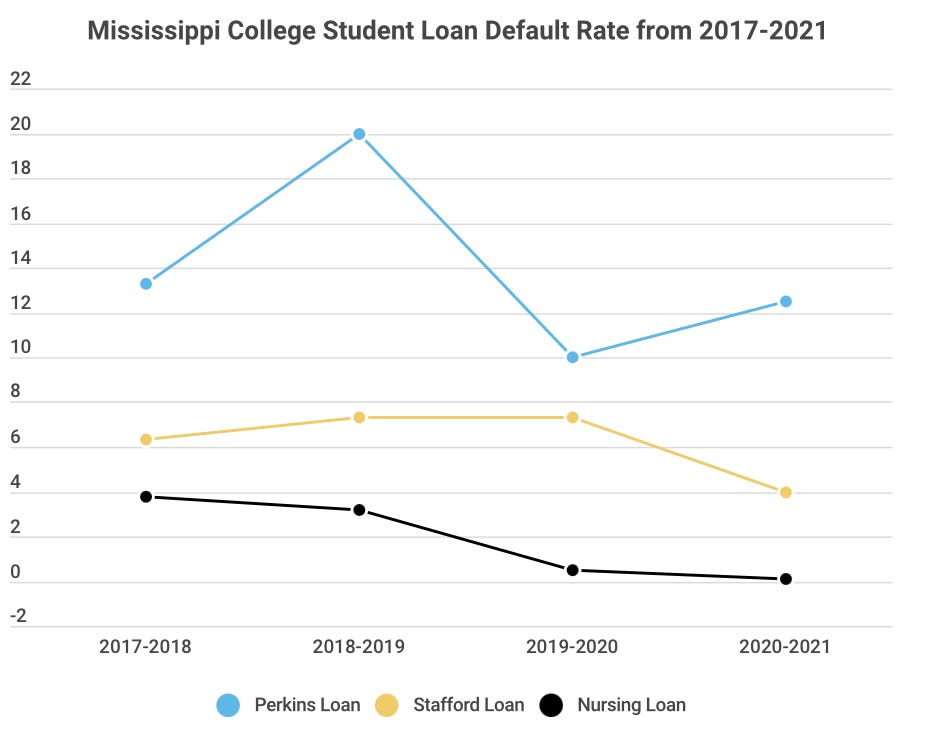

MC’s Institutional Data for Student Success shows that many of its students are not vulnerable to federal student loan default, in which a borrower is financially unable to pay back their accrued debt to lenders. Only a small percentage of student loans taken out to pay for education at Mississippi College are not paid back in accordance with the borrower-lenders’ agreements.

With the university’s established goal rate of the Perkins Loan being 9.68%, the Stafford Loan being 4.68%, and the Nursing Loan being 0.10%, the student loan default rate for the Stafford and Nursing loans hit the objective, while the Perkins loan rate was slightly higher with its most recently updated metric being about 2% more than the goal rate.

“College doesn’t have to be as expensive as it is. At MC for example, at baseline, the cost of attending is approximately $30,000 a year, and with scholarships and financial aid, it’s about $15,000. And with the available grants, you can knock that down even more. But, say you’re looking at a fee bill and wondering what each little $50 fee here and there goes toward. I think its important to ask what is my money being attributed to, where is the money going,” said Talazac.

“So, I think a lot of universities are sitting a ton of money they could be giving back to students. As a nation too, I think it’s very possible to set a new standard for average tuition rates. Look at the model of other countries: they have fewer fees and are generally just cheaper and more efficient. Their government then doesn’t see the need for student loan forgiveness on a nationwide level because their institutions are not as expensive.”

Talazac’s research for her public speaking project included sifting through copious amounts of information on the devastating effects of student loan debt, stating that its one of the leading stressors of Americans’ mental health and financial stability today, that it can halt future plans for some people, and stops them from buying a house or starting a family sooner.

The general consensus from some of those most affected by legislation was that a more targeted approach at getting the ones most vulnerable to crippling student loan debt is the answer.

It appears that simply forgiving loan debt isn’t the solution some students think is the right one for rising tuition rates.

However, there are many resources available for anyone struggling with the weight of student loan debt on the Department of Education’s official website www.studentaid.gov. The Biden administration’s plan may be the answer for some, too.

|

|